Paying your team correctly is an essential part of running a retail business.

Whether you have two employees or 20, payroll comes with legal obligations, record‑keeping requirements and deductions you must make each pay cycle.

This overview covers the key things retailers need to consider when paying employees–from tax deductions to leave, allowances to KiwiSaver obligations.

What deductions employers need to make

Every pay cycle, retailers need to make certain deductions from employees’ wages. You generally cannot deduct money from wages unless it is required by law (mandatory deductions), or the employee has given written consent (voluntary).

Mandatory deductions

Voluntary deductions

Deductions may be made from wages owing to the employee as long as both you and your employee have agreed to make those deductions. These deductions must be agreed in writing and signed by both parties.

Even if your employment agreement includes a clause that authorises the employer to make deductions in cases of overpayments or other incurred costs, you are still required to consult with employees before making a deduction from their wages.

Paying employees for leave and public holidays

Retail often involves variable hours, weekend work and public holidays, so it’s important to get leave calculations right.

Different types of leave require different calculations. Below are the main types of leave calculations.

Relevant Daily Pay (RDP) is what the employee would have earned if they worked that day. It includes base pay, commissions, incentives, overtime, and benefits they would normally get on that day.

This method is best for employees with fixed hours and clear daily rates. It is also the default payment calculation.

If the employee’s daily pay varies too much to calculate a “relevant” rate, then you can use Average Daily Pay (ADP) (below).

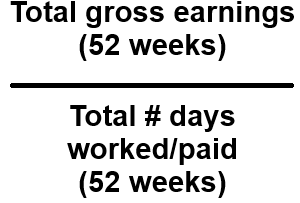

Average Daily Pay (ADP) is the employee’s total gross earnings from the past 52 weeks divided by the number of full or part days worked or paid.

This method is best for with irregular or variable hours or where it’s not practical to work out what they would have earned that specific day.

Note that RDP (above) should be used by default; you should only use ADP if the employee’s daily pay varies too much to calculate a “relevant” rate or if their employment agreement specifically allows for it.

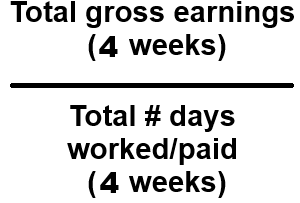

Ordinary Weekly Pay (OWP) is the higher of either:

- What the employee normally receives for an ordinary week, including base pay, commissions, incentives, overtime, and benefits they would normally get, or

- Average earnings from the last four weeks

The four-week earnings average would be appropriate for employees who may have worked overtime or covered extra shifts, etc.

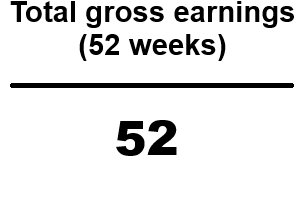

Average Weekly Earnings (AWE) is the average of the employee’s gross earnings over the 12 months (52 weeks) prior to the end of the last pay period.

If an employee has guaranteed minimum hours and works fewer than their contracted hours in a pay period, there should be some type of leave recorded to cover the unworked time.

If no leave is recorded, you are generally required to pay their minimum contracted hours even if work was not available.

If the employee asked for time off, instruct them to request the correct leave type in writing or in your leave management system so it is clear the shortfall was due to their request, not a failure to offer their guaranteed hours.

Leave and holiday payments guide

| Type of Leave | Correct Payment Type | Notes |

| Annual leave | OWP or AWE | Use whichever is higher at the time the leave is being taken. |

| Sick leave | RDP or ADP | RDP by default; ADP only if RDP cannot be calculated. |

| Bereavement Leave | RDP or ADP | RDP by default; ADP only if RDP cannot be calculated. |

| Family violence leave | RDP or ADP | RDP by default; ADP only if RDP cannot be calculated. |

| Alternative holiday | RDP or ADP | RDP by default; ADP only if RDP cannot be calculated. |

| Parental leave | Unpaid | Employees can apply for income support from IRD |

| Jury service leave | Unpaid | Employees can request to use paid annual holidays instead of unpaid jury service leave; employers cannot require this. |

| Public holidays (worked) | RDP or ADP x 1.5 | If it’s an otherwise working day, the employee also earns an alternative holiday |

| Public holidays (not worked) | RDP or ADP | Only paid if it’s an otherwise working day for that employee |

Understanding allowances

Allowances are payments made on top of regular wages for specific reasons. They may be ongoing or temporary, and they are usually set out in an employment agreement. In some cases, they can also be agreed for a short period to cover special circumstances.

Different types of allowances are taxed in different ways. If you plan to include an allowance in a job offer or retention arrangement, it is important to understand how it will be treated for tax purposes before making commitments. In general:

- Accommodation provided as part of someone’s pay is usually taxable income

- Accommodation for temporary work travel is usually not taxable

- Meal or clothing allowances that are necessary for the job are generally tax free

- Travel allowances for regular commuting are usually taxable

- Travel allowances for unusual or one‑off situations, such as getting home safely after late work, are usually not taxable

- Allowances for taking on extra duties or covering different tasks are treated as taxable income

Bonuses and Fringe Benefit Tax

Fringe benefits are non‑cash benefits provided by an employer to an employee, or to an associate of an employee, that are taxed under the Fringe Benefit Tax (FBT) rules rather than through PAYE.

They typically involve the private use of goods, services, or assets, and are separate from salary, wages, and cash allowances.

Fringe benefits may be provided on a discretionary or contractual basis.

Employers are required to apply a Fringe benefit tax (FBT) when the following benefits are supplied to employees or shareholder-employees:

- motor vehicles available for private use

- low interest/interest-free loans

- free, subsidised or discounted goods and services

- employer contributions to sick, accident or death benefit funds, superannuation schemes and specified insurance policies (excluding employer contributions to superannuation schemes liable for ESCT (formerly SSCWT)

- unclassified fringe benefits

Employers must register for FBT and pay tax on benefits provided to employees or shareholder-employees. You’ll have to file an FBT return either quarterly or annually, depending on the election made, and make any payments due.

Payday filing

You must file employment information every time you pay your employees. This is based on the date you pay employees (payday) and may be weekly, fortnightly, monthly or more often if you have multiple paydays. You only need to file employment information for an employee when you pay them.

- Employers with total annual PAYE and ESCT of $50,000 or more must file electronically.

- If your PAYE and ESCT combined is less than $50,000, you can choose to file electronically or by paper.

You can add employment information in myIR by entering the information into an online form or uploading a payroll file. You can also file directly using your payroll software.

Where retailers can get support

Payroll can be complex, especially in fast paced retail environments with varied hours and a mix of permanent and casual staff. Getting payroll right protects your business, supports your employees and helps avoid costly compliance issues.

Retailers can reduce risk by:

- Using payroll software that automatically calculates deductions, like our partner, iPayroll

- Reviewing Inland Revenue’s guidance and calculators

- Seeking support from Retail NZ by contacting our Advice Service on [email protected] or 0800 472 472 (1 800 128 086 from Australia)